AI/ML Engineer Data Science Quantitative Finance

Public Projects (6)

FIFA Cup France vs Senegal ML Prediction Model

Multi-feature logistic regression with competition importance weighting (World Cup and tournament matches weighted up to 3× higher than friendlies) and exponential recency decay applied to match history pulled from football-data.org. Wraps the model in Platt scaling via CalibratedClassifierCV for better-calibrated probabilities, pulls squad size from the teams endpoint as a depth feature, and runs a sensitivity analysis sweeping the WC weight multiplier across 7 values. Outputs form trend charts, competition mix breakdown, aggregate stat comparisons, and a sensitivity curve for their June 16 World Cup 2026 Group I matchup.

Quant Kavin

Jun 8, 2026

FIFA World Cup Brazil vs Morocco Prediction Model

Fetches full match history for Brazil and Morocco from football-data.org and applies exponential time-decay weighting to prioritize recent form. Builds Poisson attack/defense strength ratings to generate a scoreline probability grid, trains a logistic regression on recency-weighted differential features, then blends both models into a final win/draw/loss probability for their June 13 World Cup 2026 Group C clash. Outputs a scoreline heatmap, blended probability bars, and expected goals comparison.

Quant Kavin

Jun 8, 2026

FIFA World Cup USA vs Paraguay ML Prediction Model

Pulls recent international match history for USA and Paraguay via the football-data.org free API, engineers rolling form features (win rate, goals for/against, goal difference) over an 8-game window, and trains a logistic regression to output head-to-head win probabilities for their June 12 World Cup 2026 Group D opener. Includes feature coefficient analysis and a rolling form comparison chart.

Quant Kavin

Jun 8, 2026

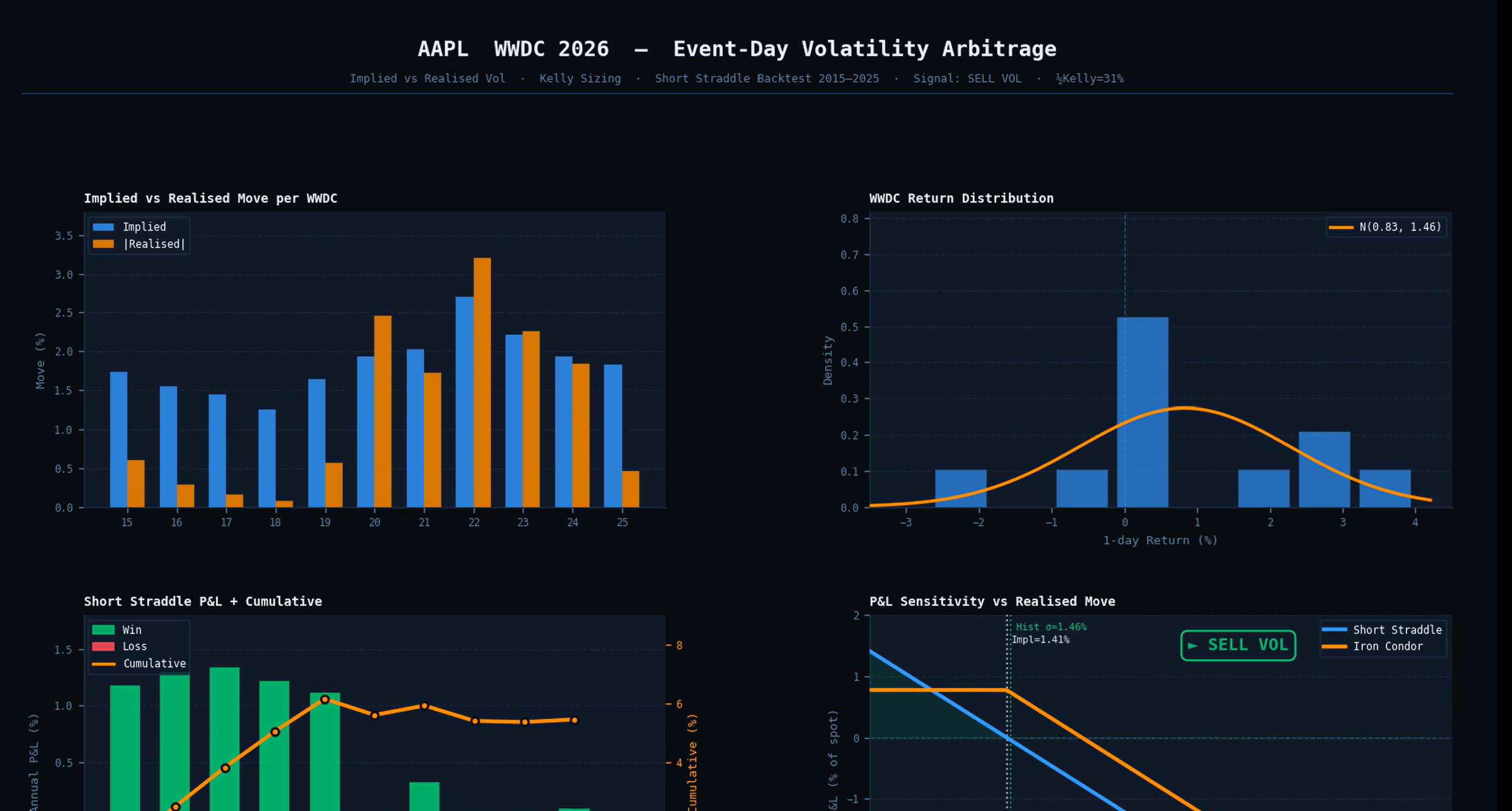

Apple WWDC Price Prediction Options Project

AAPL WWDC 2026 — Event-Day Volatility Arbitrage A quantitative options strategy built around Apple's annual WWDC keynote (June 8, 2026). The core idea is implied vs realised volatility arbitrage — options markets have historically overpriced AAPL's expected 1-day move on keynote day, creating a structural edge for volatility sellers. By collecting 11 years of WWDC event-day returns (2015–2025), comparing them against the ATM straddle implied move, and backtesting a short straddle strategy, we quantify that edge and size it using the Kelly Criterion. Quant concepts used: implied volatility, realised volatility, volatility risk premium, ATM straddle pricing (call + put ÷ spot), 1-day IV derivation (annual IV ÷ √252), Shapiro-Wilk normality testing, skewness and kurtosis analysis, Kelly Criterion position sizing (½ Kelly for safety), short straddle and iron condor payoff mechanics, Sharpe ratio, and max drawdown. Libraries: yfinance (data), pandas + numpy (analysis), scipy.stats (distribution testing), matplotlib + matplotlib.animation (static and animated charts), pillow + ffmpeg (GIF and MP4 export).

Quant Kavin

Jun 7, 2026

Maryland Keychain .STL File

Maryland Keychain I made 8 years ago. Keep in mind your filament diameter and file size, as there is small text on this keychain. Enjoy!

Quant Kavin

Jun 7, 2026

Phone Adapter Charging Case

Some old 3D printing files I made almost 10 years ago (unc). I didn't know where to upload this publicly, so I posted it here. Feel free to print and use it yourself!

Quant Kavin

Jun 7, 2026